Security of Tenure Puts Tenants in Control

EXIT Realty Matrix

Ontario tenants already have strong eviction protections; landlords can't evict tenants and tenants can remain in their units until the LTB issues eviction orders.

Read More

1. Strong documentation is essential - Leases, rent receipts, and bank records prove stable rental income and help avoid delays.

2. Lenders assess both property and risk - They evaluate rental stability, vacancy risk, and property condition when determining borrowing capacity.

3. Complete financial picture matters - Credit, savings, debts, and property details all strengthen your application and improve approval chances.

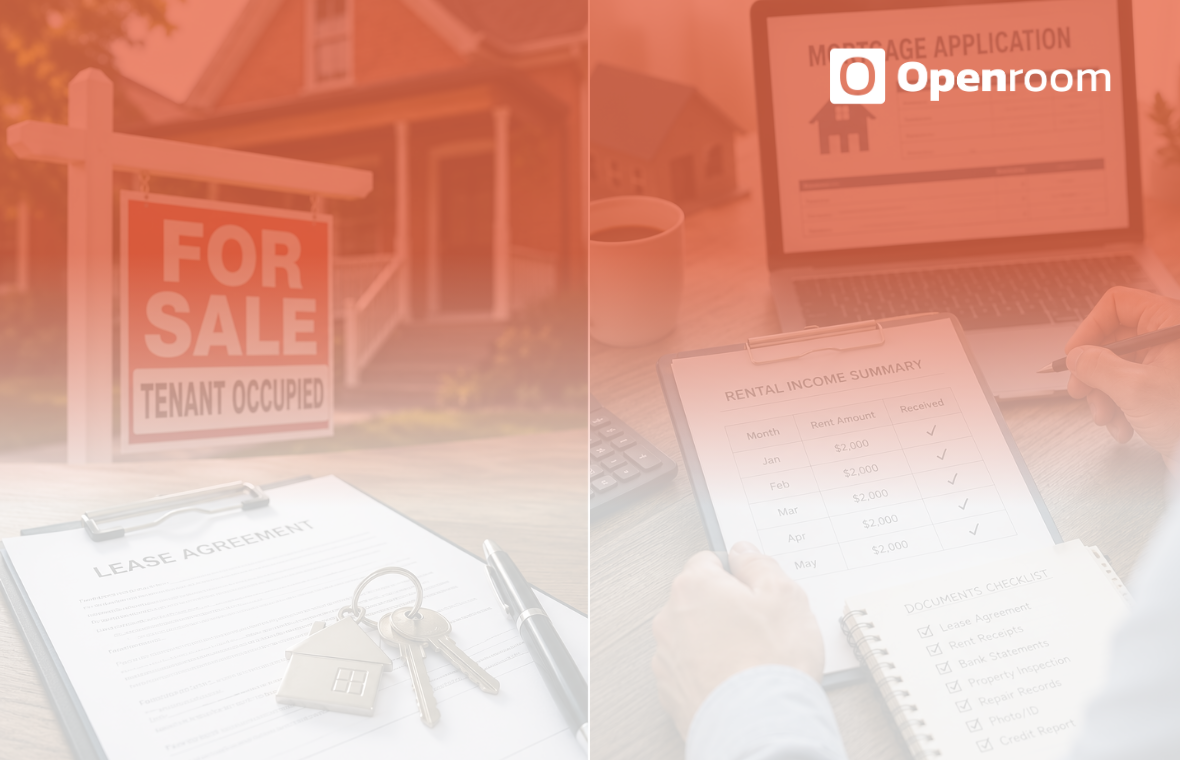

Buying a house in Ontario that already has tenants is different than buying an empty home. You need a more detailed mortgage application because lenders look at both the house price and how steady the rent money is. Your application structure is what makes the approval process go smoothly when people are already living there under lease agreements.

Lenders in Ontario look at these houses differently because rent can change how much money you are allowed to borrow. They usually check if the rent is steady, has legal paperwork and covers enough of the mortgage. It is important for you to show exactly how the house makes money.

Your application should show how the house meets what mortgage broker Mississauga lenders want. You need to show the risk of the house being empty, the history of rent payments and what shape the building is in. Lenders want to be sure the investment works even if tenants move out, which is how they decide your qualifying income.

Good applications start with organized paperwork - You should include current leases, rent receipts and bank records that show the rent being deposited - these papers prove to the lender that the money is real and not just a guess.

You should also include a summary of the rent history if new people just moved in. Lenders might ask for old rent amounts to see if the income stays the same over time. Having clear papers prevents delays and makes the lender feel better about your ability to manage the house.

Lease agreements are a big part of how lenders judge these properties. Your application is complete when it has signed leases that show the rent price, how long the lease lasts and what the tenant is responsible for - these facts help lenders see that the money is secure and follows the law.

Tell the lender if the house has rent control or if the tenants have specific legal protections. Lenders want to know if there are rules about raising the rent or moving tenants out, since the things affect your future cash flow.

A good application includes other financial facts besides just the rent. You should show your savings, credit score and any money you already owe. Lenders use this to see if you are financially stable.

Adding details like home inspections, repair records and recent updates helps your file too - these things show the house is in good shape - this makes the lender less worried about surprise repair costs that might get in the way of rent.

Working with experts can help you set up your application better. A mortgage broker is someone who shows your rental income in a way that lenders like. They can point out strengths in your application that you might not see, which is helpful if you have many tenants or complicated leases.

Investors often use mortgage broker to understand local rules and find lenders who know about Ontario rentals - this person helps you compare your options, explains what papers you need and puts your application in a better position to be approved.

Setting up a mortgage application for a house with tenants in Ontario takes focus on paperwork and rent details. If you present everything clearly with full records, lenders can accurately check your finances and the property - this is how you get a smooth approval.

Anonymous Contributors are members of the Openroom Community. Everyone is welcome to submit an Opinion Piece into Openroom because sharing stories with the wider community means we can all learn from the past to map our future paths.

_________________________

About Opinion Contributions:

Openroom seeks out the best stories around our community to elevate their voice. Each Opinion article is sent in by a genuine Openroom Community member.

The views, thoughts, and opinions expressed in the text are of the Guest Author, and do not necessarily represent the opinions of Openroom. Read more about our Opinion Contributions.

.png)

%20(1).png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)